MAKE YOUR FREE Loan Agreement

What we'll cover

What is a Loan Agreement?

When should I use a Loan Agreement?

- you intend to lend money to either a company, partnership or LLP, or

- your company, partnership or LLP intends to borrow money from someone else

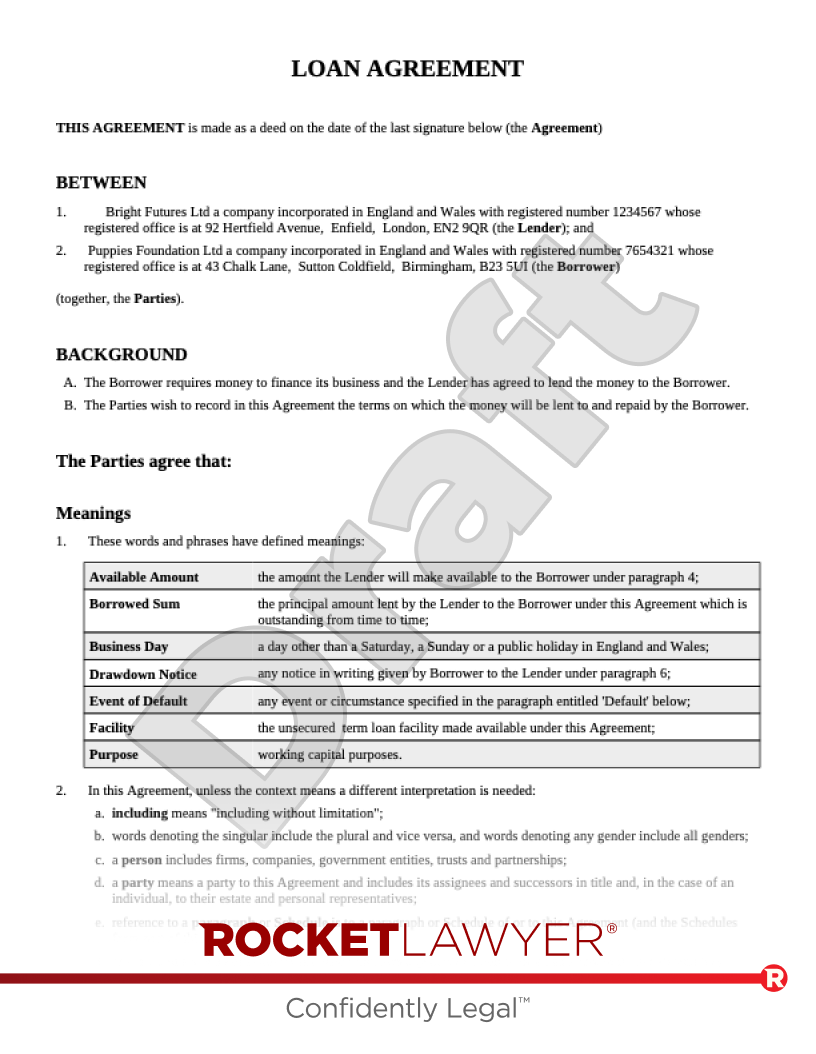

Sample Loan Agreement

The terms in your document will update based on the information you provide

LOAN AGREEMENT

THIS AGREEMENT is made as a deed on the date of the last signature below (the Agreement)

BETWEEN

(together, the Parties).

BACKGROUND

- The Borrower requires money to finance its business and the Lender has agreed to lend the money to the Borrower.

- The Parties wish to record in this Agreement the terms on which the money will be lent to and repaid by the Borrower.

The Parties agree that:

Meanings

- These words and phrases have defined meanings:

Available Amount the amount the Lender will make available to the Borrower under paragraph 4; Borrowed Sum the principal amount lent by the Lender to the Borrower under this Agreement which is outstanding from time to time; Business Day a day other than a Saturday, a Sunday or a public holiday in England and Wales; Drawdown Notice any notice in writing given by Borrower to the Lender under paragraph 6; Event of Default any event or circumstance specified in the paragraph entitled 'Default' below; Facility term loan facility made available under this Agreement; Purpose - In this Agreement, unless the context means a different interpretation is needed:

- including means "including without limitation";

- words denoting the singular include the plural and vice versa, and words denoting any gender include all genders;

- a person includes firms, companies, government entities, trusts and partnerships;

- a party means a party to this Agreement and includes its assignees and successors in title and, in the case of an individual, to their estate and personal representatives;

- reference to a paragraph or Schedule is to a paragraph or Schedule of or to this Agreement (and the Schedules form part of this Agreement);

- reference to a statute or statutory provision includes any modification of or amendment to it, and all statutory instruments or orders made under it; and

- reference to writing or written includes faxes and email but not any other type of electronic communication.

- The headings in this Agreement are for convenience only and do not affect its meaning.

Loan

- The Lender will make available to the Borrower term loan facility of an amount up to (£) (the Available Amount) on the terms and subject to the conditions of this Agreement.

- The Facility will be available for drawdown in a single instalment until from the date of this Agreement.

Drawdown

- The Borrower will draw down all or part of the Facility by giving the Lender not less than Business Days' notice in writing specifying:

- the amount (not exceeding the Available Amount) it wishes to draw down; and

- the requested drawdown date,

- Any part of the Available Amount which is not drawn down under the Drawdown Notice will be automatically cancelled.

Purpose

- The Borrower will use any amount borrowed under this Agreement solely for the Purpose.

- The Lender has no obligation to check how any amount lent under this Agreement is used.

Condition to Drawdown

- The Lender will only be obliged to make the Facility available to the Borrower if on both the date of the Drawdown Notice and the drawdown date specified in the Drawdown Notice the warranties in the paragraph entitled 'Warranties' below are true and correct in all material respects and will be true and correct in all material respects immediately after the Lender has lent the amount specified in the Drawdown Notice.

Repayment

- The term of the Facility is

- The Borrower will repay the Borrowed Sum in equal instalments of £ on the last Business Day of each calendar with the first repayment to be made on .

Warranties

- The Borrower warrants to the Lender on the date of this Agreement that:

- it is a incorporated and validly existing under the law of ;

- it has the power and authority to execute and perform this Agreement;

- it has the power to own its own assets and carry on the business it conducts on the date of this Agreement;

- its obligations under this Agreement and any transaction contemplated by it are legal, valid, binding and enforceable;

- the execution and performance by the Borrower of the obligations in and transactions contemplated by this Agreement do not and will not conflict with its constitutional documents or any of its obligations to any third party;

- it has taken all necessary action and obtained all necessary authorisations to enable it to execute, deliver and perform its obligations under this Agreement;

- no Event of Default has occurred, is continuing or might reasonably be expected to result from the Lender making any loan under this Agreement or the entry into, the performance of, or any transaction contemplated by this Agreement;

- it is not a party to any existing, pending or anticipated litigation, arbitration or administrative proceedings;

- there is no outstanding judgement or award against it given by a court, an arbitrator or any other body;

- all financial statements relating to the Borrower supplied by or on behalf of the Borrower to the Lender give a true and fair view of the Borrower's financial condition and operations on the date as at which they are stated to be drawn up;

- all information (other than financial statements) supplied by or on behalf of the Borrower to the Lender in connection with this Agreement was complete, true and accurate in all material respects at the time it was supplied or at the date it was stated to be given (except where it has been amended, superseded or updated by more recent information supplied by or on behalf of the Borrower to the Lender); and

- it is not aware of any steps having been taken or any legal proceedings initiated or threatened against it for its winding-up, dissolution or reorganisation or for the appointment of a liquidator, receiver, administrative receiver or other similar officer in respect of the Borrower or any of its assets.

- Each of the warranties in the above paragraph is deemed to be repeated by the Borrower on the date all or part of the Facility is actually lent to the Borrower by Lender under the Drawdown Notice.

Undertakings

- From the date of this Agreement, until all its liabilities under this Agreement have been discharged, the Borrower will:

- deliver to the Lender a copy of its audited financial statements within 180 days after the end of each of its financial years;

- provide the Lender with any financial or other information relating to the Borrower or its business as the Lender reasonably requests from time to time;

- notify the Lender of any litigation, arbitration or administrative proceedings as soon as it becomes aware of them;

- comply in all respects with all laws if failure to do so would have or would be reasonably likely to have a material adverse effect on its business, assets or condition, or its ability to perform its obligations under this Agreement;

- notify the Lender of any Event of Default or an event or circumstance which would (with the expiry of a grace period, the giving of notice and/or the making of a determination) be an Event of Default (and the steps, if any, being taken to remedy it) promptly on becoming aware of its occurrence;

- will not make any material change to the nature or scope of its business as carried on at the date of this Agreement;

- will not sell, lease, transfer, loan or otherwise dispose of any of its assets other than in the ordinary course of its day-to-day trading activities of the Borrower; and

- will not create or permit to subsist any security interest over any of its assets.

Default

- For the purposes of this Agreement each of the following events or circumstances is an Event of Default:

- the Borrower fails to pay any sum payable under this Agreement on its due date;

- the Borrower fails to comply with any provision of this Agreement (other than by failing to pay) unless the failure to comply is, in the reasonable opinion of the Lender, capable of remedy and is remedied within 14 Business Days of the earlier of:

- the Lender giving notice to the Borrower of the default and the remedy required; and

- the Borrower becoming aware of the default;

- any warranty or statement made or deemed made by the Borrower in or under this Agreement and/or any other document delivered by or on behalf of the Borrower in connection with this Agreement is or proves to have been untrue, incorrect, incomplete or misleading in any material respect when made or deemed to be made.

- any indebtedness of the Borrower is not paid when due;

- any indebtedness of the Borrower becomes or is declared to be due and payable before its stated maturity;

- any commitment for indebtedness of the Borrower is cancelled or suspended by a creditor of the Borrower because of any Event of Default; or

- the Borrower is unable or admits inability to pay its debts as they fall due;

- the Borrower begins negotiations with any of its creditors to reschedule any of its indebtedness because of actual or anticipated financial difficulties;

- the value of the Borrower's assets is less than its liabilities (taking into account contingent and prospective liabilities);

- any action, proceedings, procedure or step is taken relating to:

- the suspension of payments, moratorium of any indebtedness, winding-up, dissolution, administration or reorganisation (using a voluntary arrangement, scheme of arrangement or otherwise) of the Borrower;

- a composition, compromise, assignment or arrangement with any creditor of the Borrower; or

- the appointment of a liquidator, receiver, administrative receiver, administrator, compulsory manager or other similar officer in respect of the Borrower or any of its assets;

- a distress, attachment, execution, expropriation, sequestration or similar legal process affects any of the Borrower's assets;

- any provision of this Agreement is or becomes invalid, unlawful, unenforceable, terminated, disputed or ceases to be effective or have full force and effect; or

- the Borrower ceases or threatens to cease to carry on all or a substantial part of its business.

- On the occurrence of an Event of Default, or at any time after the occurrence of an Event of Default which is continuing, the Lender may by notice to the Borrower:

- cancel the Facility (which will then be immediately cancelled);

- declare that all or part of the Borrowed Sum and all other amounts outstanding under this Agreement is immediately due and payable (which will then become immediately due and payable); and/or

- declare that all or part of the Borrowed Sum becomes payable on demand (which will then become immediately payable on demand by the Lender).

- All payments made to the Lender in discharge of the Lender's indebtedness will be credited to the repayment of the Borrowed Sum.

- The Borrower will within three Business Days of demand indemnify the Lender against any cost, loss or liability incurred by it as a result of the occurrence of an Event of Default.

Entire Agreement

- This Agreement contains the whole agreement between the parties relating to its subject matter and supersedes all prior discussions, arrangements or agreements that might have taken place in relation to the Agreement. Nothing in this paragraph limits or excludes any liability for fraud or fraudulent misrepresentation.

Assignment

- The Borrower may not assign, transfer, sub-contract, or in any other manner make over to any third party the benefit and/or burden of this Agreement without the prior written consent of the Lender.

- The Lender may assign, transfer, sub-contract, or in any other manner make over to any third party the benefit and/or burden of this Agreement.

Variation

- No variation to this Agreement will be valid or binding unless it is recorded in writing and signed by or on behalf of each of the parties.

Notices

- Any notice (other than in legal proceedings) to be given under this Agreement must be in writing and delivered by pre-paid first class post to or left by hand delivery at the registered address or place of business of the notified party, or sent by fax to the other party's main fax number or sent by email to the business email address of the chief executive or equivalent of the other party.

- Notices which are:

- sent by post will be deemed to have been received, where posted from and to addresses in the United Kingdom, on the second Business Day after the date of posting, and where posted from or to addresses outside the United Kingdom, on the tenth Business Day after the date of posting;

- delivered by hand will be deemed to have been received at the time the notice is left at the proper address; and

- sent by fax will be deemed to have been received on the next Business Day after transmission;

- sent by email will be deemed to have been received 24 hours after sending.

Miscellaneous

- The Contracts (Rights of Third Parties) Act 1999 will not apply to this Agreement and no third party will have any right to enforce or rely on any provision of this Agreement.

- Unless otherwise agreed, no delay, act or omission by a party in exercising any right or remedy will be deemed a waiver of that, or any other, right or remedy.

- Provisions which by their intent or terms are meant to survive the termination of this Agreement will do so.

- If any court or competent authority finds that any provision of this Agreement (or part of any provision) is invalid, illegal or unenforceable, that provision or part-provision will, to the extent required, be deemed to be deleted, and the validity and enforceability of the other provisions of this Agreement will not be affected.

Governing Law and Jurisdiction

- This Agreement shall be governed by and interpreted according to the law of England and Wales and all disputes arising under the Agreement (including non-contractual disputes or claims) shall be subject to the exclusive jurisdiction of the English and Welsh courts.

About Loan Agreements

Learn more about making your Loan Agreement

-

How to make a Loan Agreement

Making your Loan Agreement online is simple. Just answer a few questions and Rocket Lawyer will build your document for you. When you have all the information about the loan prepared in advance, creating your document is a quick and easy process.

To make your Loan Agreement, you will need the following information:

Party details

-

What are the lender’s details (eg name and business structure)?

-

What are the borrower’s details?

-

Details of how the lender and borrower will sign the Loan Agreement.

-

If they are a partnership, what is the name of the partner signing the agreement?

-

If they are a limited liability partnership (LLP), will one member sign in the presence of a witness or will two members sign? What are the members’ details?

-

If they are a company, will one director sign in the presence of a witness or will two directors sign? What are the directors’ details?

-

Security

-

Is the loan a secured loan?

Loan details

-

Will the loan be used for working capital or other purposes? If so, what purposes will it be used for?

-

What is the sum of the loan?

-

Will the loan be available to the borrower until a specific date or for a set number of months?

-

If the loan is available until a specific date, when is the last day the borrower can access the loaned sum?

-

If the loan is available for a set number of months, for how many months can the borrower access the loaned sum?

-

-

How many days’ notice must the borrower give the lender before withdrawing the loan (in full or in part)?

Interest

-

Will interest be charged on the loan? If so:

-

What is the annual interest rate (as a percentage)?

-

Is interest payable monthly or quarterly?

-

What is the daily interest rate for late payments under the Loan Agreement (as a percentage)?

-

Repayment details

-

How many months or years does the borrower have to repay the loan?

-

Will the borrower repay the loan in monthly instalments, quarterly instalments or in full on a specified date?

-

If the loan is to be repaid in instalments, what is the amount of each repayment instalment and when does the first instalment need to be paid?

-

If the loan is to be repaid in full on a specified date, on what date does it have to be repaid?

-

-

Can the borrower repay the loan early?

-

If yes, how many days’ notice must the borrower give the lender to repay the loan early?

-

If yes, will the borrower have to pay a fee for early repayment? If yes, what percentage of the borrowed amount is the early repayment fee?

-

Jurisdiction

-

If either party is based in Scotland, will the laws of Scotland or the laws of England and Wales apply to this agreement?

-

-

Common terms in a Loan Agreement

A Loan Agreement is essential when money is being loaned by one party to a business borrower, as it sets out the specific terms attached to the loan. As a result, Loan Agreements will typically include sections on:

-

the parties’ details - the names, addresses and other details of the lender and borrower

-

the background - sets out that the borrower requires money, that the lender is lending the money to the borrower and that the parties wish to record the terms of the loan (and its repayment) in the Loan Agreement

-

meanings - sets out what is meant by key terms such as ‘Borrowed Sum’, ‘Business Day’, ‘Event of Default’ and ‘Purpose’. It also provides interpretations for parts of the agreement (eg any reference to the singular includes the plural and vice versa)

-

the loan - sets out the sum the lender is making available to the borrower and until when this loan is available to the borrower

-

drawdown - sets out how much notice the borrower must give the lender to drawdown (ie borrow on a particular day) the loan (in full or in part)

-

purpose - sets out that the borrow may only use the loan for the purposes detailed in the Loan Agreement and that the lender is not required to check this

-

condition to drawdown - sets out the conditions that need to be met before the borrower can drawdown the loan

-

interest - sets out the interest rate payable by the borrower on the outstanding sum of the loan. It also details how interest accrues, when it is payable and the daily interest rate in the event of a default on loan repayments

-

repayment - sets out the term of the loan and how the borrower must repay the loan (ie in one payment or in instalments). It also details provisions relating to the early repayment of the loan, if the borrower is allowed to repay it early

-

security - if the loan is a secured loan (under which the borrower provides collateral to the lender to protect against non-payment), this sets this out and references the separate Security Document granting the security

-

warranties - the borrower warrants (ie guarantees) that certain conditions and statements are true. The warranties under this agreement include that the borrower’s business is incorporated and validly exists and that the borrower has the authority to enter into the loan

-

undertakings - the borrower makes certain undertakings (ie written promises to do, or not do, something) until the loan is fully discharged. The undertakings under this agreement include the borrower giving the lender a copy of its audited financial statement within 180 days after the end of its financial year

-

default - sets out the type of events that constitute a default on the loan. Examples include the borrower failing to repay (part of) the loan when it is due and the borrower failing to comply with the terms of the Loan Agreement

-

the entire agreement - sets out that the Loan Agreement (and, where relevant, the Security Document) forms the whole agreement and supersedes any previous discussions

-

assignment - sets out that the borrower cannot assign (ie transfer) the agreement to another party without the lender’s consent and that the lender may assign the agreement

-

variation - sets out that variations to the Loan Agreement will only be valid and binding if they are in writing and signed

-

notices - sets out how any notices under this agreement must be written and delivered and when they are deemed to have been delivered

-

miscellaneous - includes certain boilerplate clauses and explains the enforceability of the Loan Agreement

-

governing law and jurisdiction - sets out whether the legal systems of England and Wales or Scotland must be used to resolve any disputes. For more information, read Jurisdiction and international contracts

If you want your Loan Agreement to include further or more detailed provisions, you can edit your document. However, you may want a lawyer to review the document (or make changes) for you to ensure that the modified Loan Agreement complies with all relevant laws and meets your specific needs. Ask a lawyer for assistance.

-

-

Legal tips for making a Loan Agreement

Make sure a Loan Agreement is the right document for your situation

This Loan Agreement should be used where a loan is being given to a partnership, LLP or company only. If money is being lent to an individual (be it a private person or a sole trader), a Promissory note should be used.

Consider charging interest and how much it will be

Interest is typically charged to make the risk of giving a loan (ie of the borrower defaulting on repayments) worth taking. In order to incentivise the borrower to repay the loan on time, default interest may be charged on overdue payments, at a higher rate than normal interest. For more information, read Loans between companies.

Consider whether you want the loan to be secured on unsecured

Consider whether the situation and the sum of money being loaned may require security being taken to ensure the repayment of the loan. Generally speaking, loans for smaller amounts of money don’t require security while loans for larger amounts do. For more information, read Unsecured and secured loans.

Understand when to seek legal advice

While it’s always a good idea to have your Loan Agreement reviewed by a lawyer, there are certain circumstances in which you should seek specific advice. Ask a lawyer for advice:

-

about whether the loan should be secured and the different types of security

-

and assistance on how to prepare a separate Security Document

-

if any of the parties are based outside England, Wales and Scotland

-

Loan Agreement FAQs

-

What is included in a Loan Agreement?

This Loan Agreement template covers:

-

the loan amount

-

the purpose of the loan

-

when and how the borrower can withdraw funds

-

when and how the loan will be repaid

-

interest payable

-

early repayment

-

whether the loan is secured or unsecured

-

assurances or warranties given by the borrower

-

obligations and restrictions on the borrower to help ensure the lender will be repaid

-

circumstances in which the lender can demand immediate repayment of the loan

-

-

Do I need a Loan Agreement?

A Loan Agreement is an essential document whenever you need to lend or borrow money, for example, if you are starting a business and require working capital (ie funds for general day-to-day purposes). A simple Loan Agreement clearly outlines how and when the loan will be repaid, which ensures both parties are protected during the lending process. For more information, read Loans and promissory notes and Loans between companies.

-

What is the interest payable?

When lending money, an annual interest rate applies and is calculated based on the amount of the borrowed sum. The interest rest is payable by the borrower monthly or quarterly, and can either be a fixed percentage or a percentage above the base lending rate of a bank.

In case of late payment, another daily interest rate applies. This rate is payable from the date of non-payment to the date of actual payment. The daily interest rate for late payment is a percentage above the annual interest rate. For more information, read Calculating interest on commercial debts.

-

Can a loan be repaid early?

This Loan Agreement can include a provision allowing the borrower to repay the loan in full or in part at any time, by giving a certain notice to the lender. The lender may also require the borrower to pay an early repayment fee, which is a percentage of the borrowed amount.

-

What is the difference between a secured and an unsecured loan?

A secured loan involves the borrower putting forward a source of equity (eg a house) to act as collateral for the loan. If the borrower defaults on the loan (ie fails to pay the sum payable on the due date or fails to comply with any provision of the Loan Agreement), the lender can take steps to take ownership of the collateral. Where the loan is to be a secured loan, you will need to prepare and enter into a separate Security Document to cover the collateral. Ask a lawyer for help preparing a Security Document.

An unsecured loan is a simpler type of loan under which the borrower does not need to provide collateral. In situations involving unsecured loans, lenders are not able to take ownership of borrowers’ assets in case of a payment default.

For more information, read Unsecured and secured loans.

-

Can the lender ask for immediate repayment of the loan?

The lender can cancel the term of the loan and ask for immediate repayment in case of default by the borrower.

-

What if I’m lending money to or borrowing money to a private person?

Instead of a Loan Agreement, you should use a Promissory note if you are:

-

lending money to a private individual or sole trader

-

borrowing money as a private individual or sole trader, or

-

lending or borrowing small sums of money

A promissory note is legally enforceable; however, it is less formal than a Loan Agreement. For more information, read Loans and promissory notes.

-

Our quality guarantee

We guarantee our service is safe and secure, and that properly signed Rocket Lawyer documents are legally enforceable under UK laws.

Need help? No problem!

Ask a question for free or get affordable legal advice from our lawyer.